Specifics of assessing the value of a business in modern conditions in Russia. Modern problems of science and education Application of assessment methods in Russian conditions

The valuation of shares is one of the urgent problems modern market valuable papers Russia. This is due to many circumstances, the main of which are the following:

Variety of types of securities value;

Availability of alternative concepts for determining the value of securities and methods of calculating it;

Simultaneous influence of multidirectional factors on the level of the value of securities;

Lack of professionally trained financial market analysts;

Lack of specialized organizational structures.

Russian theory, in accordance with which stocks are valued, has changed significantly over the past decades. This theory is deeply controversial, and no stock valuation method has yet been universally accepted. Different approaches and assessment methods actual value shares are based on an analysis of the company's assets, cash flows and projected earnings. A large number of different types of share prices correspond to different approaches and valuation methods based on certain concepts.

The choice of approaches and specific methods for assessing the value of shares is determined by the professionalism and qualifications, theoretical and methodological preferences of the appraiser. Theoretically, there are two bases for assessing the value of shares, which are based on the concepts appraisal activities and the theory of stock market pricing.

Valuation base based on valuation concepts. In appraisal activities, various concepts of value are used (table).

Table - Concepts of value used in valuation activities

| Assessment approaches | Content of the concept |

| Expenditure (replacement) or property (asset accumulation) | The value of a share is determined on the basis of the replacement cost of an existing JSC (the cost of creating a similar enterprise) The value of a share is derived from the value of an existing enterprise (business). shares based on the total market value of each element of assets, adjusted for time and cost of their sale |

| Income approach | The share price is determined on the basis of: 1) discounting the current value; 2) capitalization of net profit (cash flow) |

| Comparative approach (analogy, comparison or capital market) | A share has a value comparable to the value of market sales of shares similar in type of activity, profile, amount of capital, ratios (multipliers) and other characteristic features (parameters) of JSC |

Valuation base based on theories of pricing in stock markets. Numerous pricing theories reflect different approaches to determining the value of securities. The main theories used in valuation activities are portfolio theories, functional analysis, reflexivity, market analysis and forecasts, cycles, agency relations, etc.

Table - Approaches and methods for assessing the value of shares

| Type of share price | Approach or method name | Applying an approach or method |

| Book value | Property approach (methods of accumulating assets or net assets) | Reorganization, insurance, liquidation, restructuring and collateral |

| Liquidation value | Property approach (asset accumulation method) | Reduction of the authorized capital, liquidation of the joint-stock company. Redemption, liquidation and cancellation of shares |

| Market price | Income approach (methods of discounting the future expectations of investors and capitalizing net income) | Formation of securities portfolios, forecasting profitability and determining the effectiveness of investments. Investment projects, analysis of the ratio of capitalization and net profit |

| nominal value | Cost approach | Creation of a joint stock company |

| Issue value | Cost approach | Placement of the issue |

| Conversion value | Comparative approach | Exchange of shares |

| Market value | Comparative approach | Various deals |

Topic 4. Portfolio theory and models of the value of financial assets

The concept of an investment portfolio, principles and stages of its formation. Portfolio risk and return. Optimal portfolio. Market portfolio. Capital Market Characteristic Line (CML). Financial Assets Pricing Model (CAPM). Security characteristic line (SML). Arbitrage Pricing Model (APT)

An enterprise (business) is the most difficult object of appraisal, requiring from an appraiser, in addition to mastering all methods of appraisal itself, also a certain knowledge of the basics of investment and macroeconomic analysis, familiarity with different methods of market research.

As market relations develop, the need for independent appraisal will increase. There are already legal requirements for conducting independent evaluation in a number of cases. So, according to the Federal Law "On appraisal activities in Russian Federation"assessment of objects belonging in whole or in part to the Russian Federation, constituent entities of the Russian Federation, or municipalities, is mandatory for their privatization, transfer to trust or lease, sale, nationalization, redemption, transfer as a contribution to authorized capital. The same Federal law identified cases of mandatory property valuation in the context of litigation. Both the judicial authorities and the parties involved in the proceedings have already realized the importance of independent appraisal expertise for objective consideration and delivery of a reasoned decision on a wide range of arbitration and civil claims.

The Law of the Russian Federation "On joint stock companies ah "also requires the assessment of the market value of the share capital by independent appraisers in certain situations. For example, this procedure is provided for in the case of an additional issue, redemption of shares, etc.

One of the features of the modern Russian economy is the presence of a large number of inefficient enterprises, often with large tangible assets. The restructuring of such enterprises is a rather complex process, in which there is a place for an independent assessment. Indeed, an enterprise appraisal is necessary to select a reasonable direction for its restructuring; during the appraisal process, alternative approaches to enterprise management are identified and determine which of them will provide the enterprise with maximum efficiency, and, consequently, a higher market price, which is the main goal of the owners and the task management firms in a market economy.

Independent evaluation different types the value of enterprises (market, restoration, liquidation) plays a significant role in the process of functioning of financial institutions of the market - banks, insurance companies, stock exchanges. For example, banks are often interested in assessing the market value of the collateral or in determining the liquidation value of the borrower; insurance companies, when concluding insurance contracts and paying compensation, have to determine the replacement cost of objects; stock exchanges and other participants in the stock market rely on the data of an independent appraisal of an enterprise when determining the market prices for its shares.

The growing flow of foreign investment into the Russian economy is also contributing to an increase in demand for the services of independent appraisal organizations... Investors, most of whom are from Western Europe and the United States, bring with them their understanding of the culture and methodology of implementing the investment process, in which the role of independent appraisers is much more significant than that of their Russian counterparts. But, despite the formation of conditions conducive to increasing the role of independent appraisal of enterprises among other mechanisms market economy, there are many obstacles to the development of business valuation. The main obstacles are the inaccessibility of the necessary information on the parameters of transactions for the sale and purchase of enterprises in various industries (and often the absence of the transactions themselves) and the lack of transparency in the system of maintaining financial records at enterprises. In addition, the general instability of the economy and the lack of historical information on the evaluated business often make any predictions about possible outcomes unreliable. economic activity of this or that enterprise. All this imposes serious restrictions on the applicability modern approaches to business valuation, for example, such as the comparative and profitable approach, and the experience of Russian appraisers in the field of business valuation, basically, comes down to the use of cost methods traditional for the domestic economy.

We can say that the quality of business valuation as a market service (and hence the demand for this service) in Russia will depend on the further improvement of all the mechanisms of the stock market, the increase in its activity, the formation of a mergers and acquisitions market, the emergence of available flows of necessary market information and general stabilization of the economic situation in the country.

The chapter discusses the main methodological approaches to business valuation, provides valuation methods characteristic of a particular approach, names their areas of application, and gives a comparative assessment.

Most professionals agree on the existence of three approaches to determining the value of an enterprise (business): cost, comparative and profitable.

Certain types of businesses are usually valued based on their commercial potential (for example, a petrol station or hotel). The volume of gasoline sales, the number of guests in the hotel are sources of income, which, when compared with the cost of operating expenses, allows you to determine the profitability of a given enterprise. This approach to valuation is called profitable. The income approach is a valuation procedure based on the principle of a direct relationship between the value of a company's business and the current value of its future income that will arise from the use of the property and / or its possible further sale.

If the enterprise (business) is not sold or bought, if there is no developed market for this business, when considerations of generating income are not the basis for investment (hospitals, government buildings), the assessment can be made on the basis of determining the cost of construction, taking into account depreciation and adding replacement cost taking into account wear, that is, a costly approach. The cost approach (valuation based on asset analysis) is most applicable for special purpose companies, material-intensive and capital-intensive industries, as well as for insurance purposes. Assets based valuation is based on the principle of substitution and balance.

The application of the cost-based approach is necessary in two cases:

First, the cost-based approach is irreplaceable when evaluating non-listed companies, most often registered in the form of LLCs, CJSCs, GUPs, which, as a rule, have opaque financial flows;

Secondly, the application of the cost approach together with other approaches, and above all the profitable one, allows making effective investment decisions.

In the event that there is a market for a business similar to the one being assessed, a comparative or market approach can be used to determine the market value, based on a selection of comparable properties already sold in this market. In contrast to the costly comparative approach, it is based on market information and takes into account the current actions of potential buyers and sellers.

It should be noted that in recent times Along with the traditional approaches in the domestic theory and practice of assessing the value of companies, a new - the option approach - is being actively used.

In the practice of operations with the appraisal of enterprises, there are a variety of situations. At the same time, each class of situations has its own, appropriate only approaches and methods. For the right choice methods, it is necessary to preliminarily classify valuation situations using a grouping of objects, the type of transaction, the moment at which the valuation is made, etc. Moreover, if tens or hundreds of homogeneous objects circulate on the market, it is advisable to use a comparative approach. A cost-based approach is preferable for evaluating complex and unique objects.

In an ideal market, all three approaches should lead to the same amount of value. However, most markets are imperfect, potential users may be misinformed, and manufacturers may be ineffective. For these, as well as other reasons, these approaches can provide different measures of cost.

Each of the three named approaches involves the use of methods inherent in the assessment.

Thus, the income approach involves the use of the capitalization method and the discounted cash flow (ESD) method.

The cost approach uses the method of net assets (AV) and the method of residual value (LV).

The comparative approach uses: the capital market method, the transaction method and the industry coefficient method.

The methods of discounted cash flows, capital market and industry ratios are focused on assessing the enterprise as operating and which will continue to operate. The net assets method and the transaction method, on the contrary, are applicable to the case when the investor intends to close the enterprise or significantly reduce the volume of production. The capitalization method is reasonable to apply to those enterprises that have accumulated these assets as a result of their capitalization in previous periods; in other words, this method is most adequate for assessing enterprises that are “mature” in terms of their age. The discounted cash flow method is more applicable for evaluating young enterprises that have not managed to earn enough profits to capitalize in additional assets, but which nevertheless have a promising product and have clear competitive advantages over existing and potential competitors. Methods of capital market, transactions and industry ratios are suitable provided that a peer company is strictly selected, which must be of the same type as the company being valued.

From the analysis of the advantages and disadvantages of all of the above approaches (see generalized table. 3.1) and methods, it can be concluded that none of them can be used as a basic one. Moreover, each of them can give different, sometimes opposite, assessment results and represent the interests of various parties, for example, owners and potential investors.

The possibility (and even in many cases the necessity) of applying different methods of business valuation to the valuation of a particular enterprise in a particular investment situation leads to a rather elementary idea of “weighing” valuations calculated by different methods and summing such “weighted” valuations. In this case, the weighting coefficients of the significance of estimates for different, in principle admissible in this situation, assessment methods are understood as the coefficients of confidence in the corresponding method. These coefficients are purely expert.

| Table 3.1 Comparative analysis approaches to assessing the value of an enterprise

|

The final estimate of the value of the enterprise (business) can be determined by the formula:

where is the valuation of the enterprise (business) g-th method(all applicable assessment methods are randomly numbered); r -1, ..., n - the set of assessment methods applicable in this case; is the weighting factor of the method number and

Obviously, at the same time, the reasonable setting of the coefficients is one of the main evidence of the sufficient qualifications and impartiality of the business appraiser.

The need for an assessment Russian companies currently Associated with the redistribution of property privatized in the early 1990s. The problem is that the direct application of classical methods of assessing the value of a business to Russian enterprises is difficult due to objective reasons. These include:

Underdevelopment of the Russian securities market (at present, it is actually absent), as a result of which there is no information on the market quotation of the securities of the evaluated enterprise;

Informational closeness of the Russian market - in some cases it is impossible to get a public financial statements even open joint-stock companies, which makes it difficult to collect information on similar companies;

Measured by hundreds and thousands of items, the range of products manufactured by Russian industrial enterprises. This also makes it difficult, and sometimes even makes it impossible to find analogues of the evaluated enterprise not only in our country, but also abroad;

Most of the evaluated enterprises show profits close to zero, which is a consequence of tax evasion, or they are generally unprofitable, which is a consequence of the general state of the economy in the country or a consequence of ineffective management. Thus, using the discounted cash flow approach is also problematic;

The significance of the factors involved in the formation of the value of the enterprise is different. Abroad, a resource such as land loses its dominant importance when considering business. For Russia, the land or location factor plays a significant role (these are the large size of the enterprises themselves, the remoteness of raw material suppliers, the availability of appropriate infrastructure in the region);

The presence of a layer of shareholders who received shares free of charge or almost free of charge in the course of privatization.

The incriminating feature of the Russian economy at the present time is its instability. The risks faced by entrepreneurs in Russia are much higher than the average values typical for countries with developed market relations. The situation is aggravated by high inflation rates, which lead to the fact that the little information that can be obtained (or that is available) to assess the value of an enterprise, reflects the business in "distorting mirrors". Inflationary processes affect the position of the enterprise: they underestimate the value of the enterprise's property; accumulation of money for capital investments becomes impossible; the short-term interests of the enterprise dominate, etc.

When evaluating Russian enterprises the date of the assessment is of particular importance. Linking the assessment to time is especially important when, on the one hand, the market is oversaturated with property in a pre-bankrupt state, and lacks investment resources, on the other hand. The Russian economy is characterized by an excess of the supply of all assets, including real estate, over effective demand. This supply-side imbalance directly affects the expected value of the property being offered for sale. The price of property in a balanced market does not match the price in a market depression. But property owners and investors are interested in the real price that will be offered in a specific market, at a specific moment and in specific conditions. Buyers seek to reduce the likelihood of losing their money and require certain guarantees. Therefore, when determining the price of an enterprise, it is necessary to take into account all risk factors, including the risk of inflation and bankruptcy.

The use of a comparative or market approach to assessing an enterprise in our country is limited due to the impossibility of obtaining objective information for comparison.

At first glance, in an inflationary economy, the method of the present value of the enterprise (the method of discounted cash flows) is most suitable for evaluating an enterprise, since the percentage of inflation is taken into account in the discount rate. But this is possible if the rate of inflation is predictable and the economy is functioning normally. It is very difficult to predict the flow of net income from the activities of an enterprise for several years ahead in an unstable economy.

V modern conditions business valuation is a necessary step for the further development of an economic entity. This is due to the fact that the assessment allows you to determine how effectively the company operates in the market environment and, if there are problems, to quickly eliminate them and thereby increase the stability of the business.

The development of a market economy has led to the formation of enterprises of various forms of ownership. The owners have the opportunity to advance the available free cash into a business, to sell it. Thus, business has become a kind of commodity that must have a price.

Business valuation in Russia is understood as professional activity subjects of appraisal activities aimed at establishing market, cadastral, liquidation, investment or other appraisal of value in relation to appraisal objects

Also, the assessment of the value of a business is a procedure for calculating the market value of an economic entity, taking into account its assets and financial results, which is carried out by specialized organizations or authorities.

Today, ensuring sustainable business development is associated with the analysis of business processes occurring at the enterprise, an analysis of the strengths and weaknesses subject, as well as monitoring the competitive environment.

Considering the models for assessing the value of a business, it can be noted that initially they were focused on a "hard" scenario for the development of an economic entity and practically did not take into account the specifics of the "problems of a cognizing subject" - the flexibility or quality of management decisions.

Analyzing the existing methods for assessing the value of a business, it should be noted that many of them do not take into account the mechanism of a market nature, which is inherent in certain countries, this statement is true for the Russian Federation.

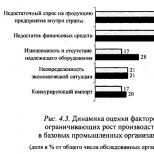

Among the national characteristics of assessing the value of a business in the Russian Federation, the following can be noted:

- Inefficient operation of the stock market, which leads to errors in the results of evaluating certain processes. In Russia, I have formed a system of indicators that allows me to fully assess the trends in this area.

- There is a high level of uncertainty in the market, the presence of which is due to the unpredictability of price changes in the long term.

Evaluation activity is an important part of the implementation of the process of reforming the country's economy and the formation of the rule of law. This type of activity makes it possible to form an information basis for restructuring the economy and ensure the formation of a competitive market environment. Through the assessment, objective information is formed about the economic processes taking place in the economy.

Today the following problems of appraisal activity in the Russian Federation can be identified.

- The scoring system is not linked to the system accounting and taxation, which does not allow the formation of a harmonious system for assessing the value of an economic entity.

- Lack of a clear system of interaction between auditors, appraisers and specialists in financial consulting.

- Poorly designed assessment methodology

However, today the methods of business valuation are being modernized. In addition to traditional approaches, new methods are being introduced based on the use of various financial instruments.

As effective tool business growth in modern conditions is recognized as a real option. Often a real option is understood as the practice of applying the theory financial options to the management of real assets. The essence this method business valuation consists in assessing, calculating the optimal value and determining the prospects for the development of an existing business. Business valuation using the real option method allows you to make the necessary adjustments to the value of a business that was previously estimated according to a rigid scenario.

We will develop a business valuation model using the real options method. The data are presented in Figure 1.

Figure 1. A business valuation model using the real options method

In accordance with the figure, we can conclude that the initial step in assessing the value of a business is to determine the objectives of the assessment. It is the goals that set the vector of analysis and justify the use of certain assessment methods.

Based on the results of the assessment, a report is drawn up, according to which it is possible to determine the possible development reserves of the entity, which will contribute to the growth of its value.

The assessment methodology needs to be improved, as well as to adapt the improved methods to the realities of Russian companies. As methods for improving the methodology of analysis, it is possible to propose to create an approach that would combine analysis internal environment company and external components. This would allow more factors to be taken into account when assessing the business, and the investigator would more accurately and fully determine the value of the company.

The following promising goals for the development of appraisal activities in the Russian Federation can be distinguished:

- The short-term goal is to form a complete regulatory and legal framework that will provide comprehensive regulation of valuation activities and the activities of appraisers.

- The strategic goal is the formation of such a system of valuation activities that could adapt to changing conditions and develop under the influence of various factors. This would ensure the provision of high-quality business valuation services, which would improve the level of business valuation in Russia and make it competitive in comparison with the international level.

Among the innovations in appraisal activities in 2018, it is planned to create professional standard for appraisers, which has already been made public. This standard assumes the emergence of ancillary activities in the implementation of the assessment. Certain requirements will be imposed on the level of education of the appraisers' assistants.

In order to determine the cost of objects of the 1st category of complexity, the employee must have a higher education or specialized education of the same level. Work experience of at least a year.

To assess an object of the 2nd category of complexity, employees must have a specialized higher education master's or specialist's level, or non-specialized education bachelor's or specialist's degree.

Also, changes will be made to the metrological research activities in the field of business valuation.

To employees holding managerial positions, there will be a requirement: at least 3 years of work experience in managerial positions.

Also among the innovations, it can be noted that the assessors must pass the exam before April 1, 2018. Experts estimate that a total of 22,000 people are expected to complete this training in 2018.

Thus, the valuation activity develops, changes are made to regulatory framework regulating this type of activity.

Bibliography:

- Federal Law "On Valuation Activity in the Russian Federation" dated July 29, 1998 N 135-FZ [ Electronic resource] Access mode: http://www.consultant.ru/document/cons_doc_LAW_19586/ (date of access: 02.02.2018).

- Gorbunova M.A., Masalskaya M.A. Business value assessment: theoretical and practical aspects // Synergy of Science. - 2017. - No. 12 - P.21-30

- E.A. Parshkova Business valuation and management of its value // Scientific community of students of the XXI century. Economic sciences: collection of articles. Art. by mat. LIII int. stud. scientific-practical conf. No. 5 (53).

- Markova E.V., Verevichev I.I. The problem of assessing the growth of business value using real options // Basic research... - 2017. - No. 6 - P.149-153